CIO Insights: China AI – Build Now, Profits Later

Share this

10 minute read

Chinese tech stocks have rallied about 80% over the past 12 months, driven largely by investor optimism around AI. Much of the rally reflects a valuation re-rating – or a near-term revaluation of what these companies are worth. But for a sustained bull market to take hold, earnings growth will have to catch up.

In this month’s CIO Insights, we explore how China’s AI progress fits into the bigger picture for investors, and what it signals about the outlook for Chinese equities.

Key takeaways

- AI is central to China’s investment story. With tech comprising more than half of broad Chinese equity indices, and AI adoption expanding across sectors, the trajectory of the country’s AI development is critical for the long-term prospects of investing in China. It also matters for global asset allocators – as demonstrated by breakthroughs like DeepSeek-R1, which rattled tech equities worldwide. As AI is clearly the new strategic arms race between the US and China, the pace of its progress will continue to play a pivotal role in markets.

- China’s AI stack is showing rapid but uneven progress. The country has made significant progress in building out its AI infrastructure, particularly in areas like power and cloud computing. However, it remains constrained in its supply of advanced chips due to US export controls – though the development of home-grown alternatives is accelerating. On models, this year’s “DeepSeek moment” suggested China trails the US by just 1-2 years, but with an increasingly robust ecosystem of open-source models, that gap is narrowing. On the application side, monetisation is clearer in advertising, gaming, and cloud, but remains nascent in e-commerce and service platforms.

- China’s AI build-out may deliver some near-term earnings, but the path to larger-scale monetisation is still unclear. In the US, the AI rally has been powered by clear leaders like the Magnificent Seven, which are already turning adoption into profits. In China, earnings strength is visible in hardware and equipment, but most companies have yet to show that AI can drive broader profit growth. For now, heavy spending is driving the build-out, but it remains to be seen whether this will translate into meaningful profits over the coming 6-12 months.

(See our Glossary at the end of the article for descriptions of terms used.)

China’s AI advancements are shaping markets at home and abroad

For investors, China’s progress in AI matters in two ways: first, as a driver of the country’s own equity markets, and second, as a force increasingly shaping global markets.

Let’s start with Chinese equities. As Chart 1 illustrates, tech-related sectors comprise more than half of broad-based China equity indices. What’s more, the two biggest companies by market capitalisation, Tencent and Alibaba, are also at the forefront of AI.

With such a large share of the market tied to tech, the trajectory of AI developments will naturally have an outsized impact on overall index performance – making AI not just a thematic story but a structural driver of index-level returns in China. As AI becomes embedded across industries – from e-commerce to banking – its influence on China’s equity market is likely to broaden further as a wider set of companies begin reporting efficiency gains and product upgrades tied to AI.

At the same time, China’s AI progress is increasingly shaping global markets. Earlier this year, the release of DeepSeek-R1, an open-source large-language model (LLM), was a clear signal that China’s AI capabilities are catching up quickly – and potentially at a lower cost than leading US peers. This “DeepSeek moment” rattled global tech stocks, including double-digit drops for semiconductor leaders NVIDIA and Broadcom, and underscored how China’s advancements have the potential to send shockwaves through global markets.

Looking ahead, adoption is expected to accelerate sharply. As we shared earlier this year, rising tech protectionism is only accelerating the shift, with both Beijing and Washington stepping up investment across the AI ecosystem as a strategic priority. (More on this in our CIO Insights: The long view on “Liberation Day”.)

The next question then is: how far along is China in building out that ecosystem – from infrastructure, to models, to applications?

Rapid yet uneven progress defines China’s AI stack

Across its “AI stack” – the layers of infrastructure, models, and applications that support AI development – China is seeing significant progress, though some parts are advancing faster than others.

Chips: Supply remains constrained, but the gap is starting to close

US export controls continue to limit China’s access to NVIDIA’s most advanced processors, which are central to training cutting-edge AI models. However, Beijing and the country’s tech giants are moving quickly to close the gap:

- Homegrown chips are gaining traction. Alibaba and Baidu are already training models on their in-house chips. As workloads shift from training to inferencing, which demands less advanced hardware, the barrier to using homegrown chips is falling1. On the design and manufacturing side, Huawei and SMIC are narrowing the gap with NVIDIA and TSMC.

- Switching costs are falling. In the past, shifting from NVIDIA’s ecosystem to Chinese hardware required a costly overhaul of software, due to its proprietary CUDA system (the code that runs on top of their chips). Today, Alibaba’s chips are designed to run much of the same code2, making it easier for companies to migrate if supply tightens.

Power: China’s underappreciated AI advantage

Chips get the spotlight when it comes to AI, but power is just as critical. Each new generation of graphics processing units (GPUs) consumes more electricity, making grid capacity a key constraint for scaling AI.

China has invested heavily in its power generation capacity, which has grown more than tenfold since 2000, reaching 3,218 gigawatts (GW) in 2024, and is now more than 2.5 times that of the US, as illustrated below in Chart 2.

To put this in perspective, McKinsey estimates global data-centre demand will jump from about 70 GW today to 220 GW within five years3, driven largely by AI. This build-out gives China an advantage in supporting energy-hungry digital infrastructure.

Foundational models: Narrowing the gap via open source

China still trails the US on cutting-edge foundation models, but the gap is narrowing, with some estimates suggesting a lag of less than a year. As Table 1 below shows, Chinese models are competitive with their US peers across multiple performance benchmarks. While OpenAI still tops the table, strong showings from the likes of ByteDance, Alibaba, DeepSeek, and a number of start-ups highlight the pace of China’s progress.

Where China differs most is in its embrace of open source. Dozens of new models are being released, encouraged by policy support for openness and competition. This dynamic – similar to the rapid learning cycles that propelled China’s EV industry – has helped accelerate innovation and spread advances across the ecosystem.

Applications: Monetisation is still uneven

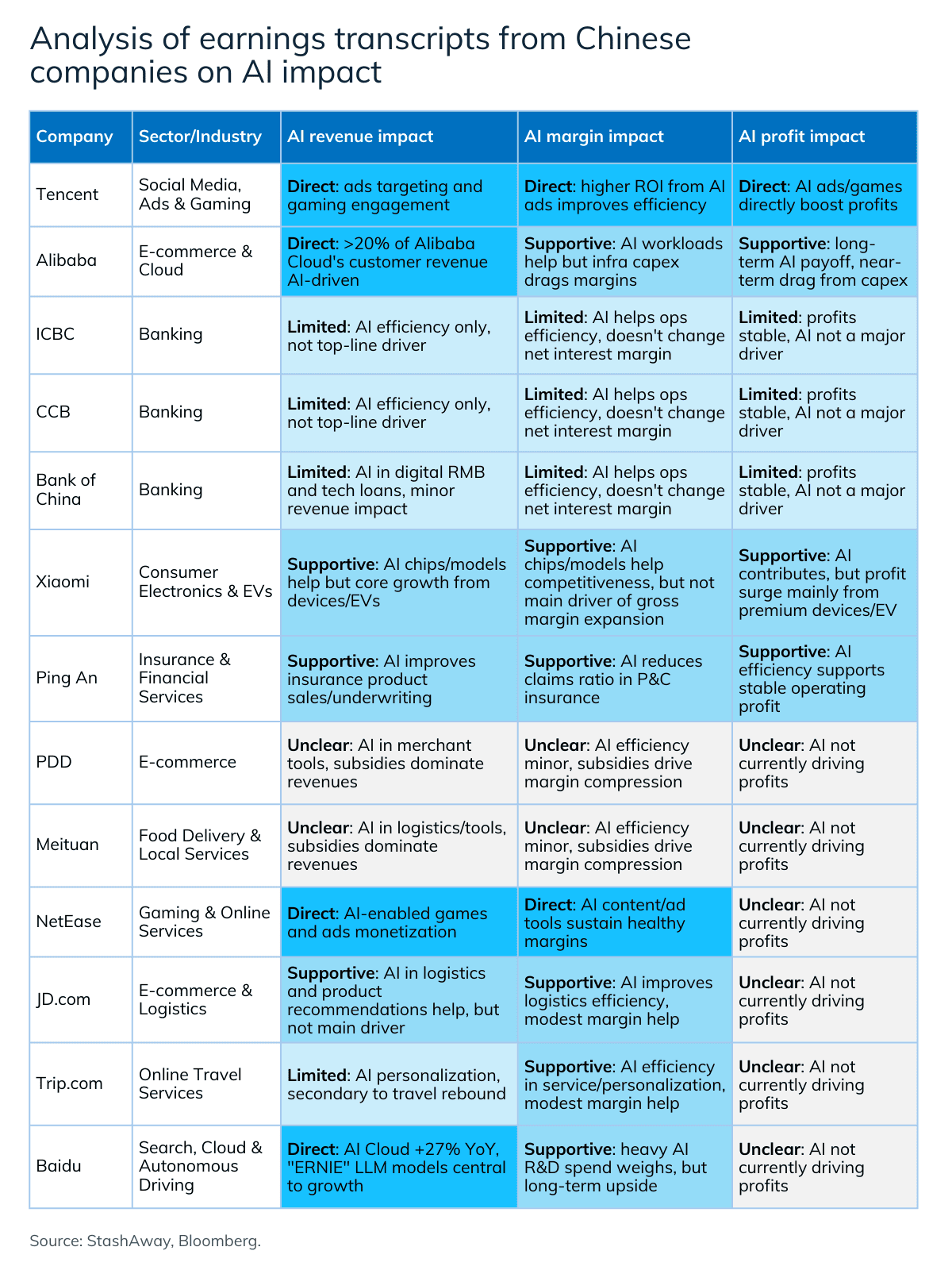

Recent earnings calls from China’s biggest companies reveal that AI is starting to support revenues, but the bottom-line impact is still being capped by heavy capex, subsidies, and competition. A few key sectors are already reporting clear gains, while many others remain in the investment and experimentation phase.

- Clearer gains in advertising, gaming, and cloud. These sectors are seeing the clearest measurable revenue uplift, with personalisation and engagement directly driving sales. On recent calls, companies like Tencent, NetEase, Alibaba, and Baidu pointed to AI as a direct growth driver in those business segments.

- Early-stage adoption elsewhere. E-commerce, consumer service platforms, and travel firms – like Meituan, PDD, JD.com, and Trip.com – are deploying AI to improve logistics, recommendations, and customer service. So far, these uses improve efficiency and competitiveness, but heavy investment means the net earnings effect is limited for now.

- Strategic expansion, but with limited earnings impact so far. Hardware makers like Xiaomi are embedding AI features into devices, while banks and insurers highlight its role in risk management and customer service. Sizable spending on R&D, infrastructure, and subsidies suggests companies are prioritising scale and capacity over near-term profit growth.

Taken together, commentary from Chinese companies – summarised in Table 2 below – highlight AI’s role in supporting revenues and efficiency, but not yet in driving broad-based profit growth. This stands in contrast to the US, where the AI rally has been powered by clear leaders like the Mag-7 already converting adoption into earnings growth.

(A more detailed table can be found in the Appendix at the end of this note.)

The trillion dollar (or renminbi) question for China: How to monetise AI

The key question is whether China’s AI build-out will deliver near-term earnings or is still laying the groundwork for longer-term returns. For now, it seems that earnings momentum is most visible in select subsectors like technology hardware and equipment, with most firms still prioritising scale and infrastructure over bottom-line returns.

Earnings strength is concentrated in tech hardware, while chips and software lag

A deep dive into sector-level earnings shows that forward earnings estimates are rising most strongly in information technology. As Chart 3 highlights, earnings-per-share (EPS) forecasts for the IT sector are up 35% year-on-year, compared with just 3% for China equities overall. This suggests that AI’s influence is being felt most in the sectors supplying the infrastructure for adoption.

Looking within the IT sector, however, the build-out is also far from even. Technology hardware and equipment is driving gains, with forward EPS growth near 58% YoY. By contrast, semiconductors & semiconductor equipment and software & services show double-digit contractions.

This divergence reflects China’s position: hardware makers supplying servers and networking gear are benefiting from AI demand, while chipmakers face export restrictions and intense competition, and software firms still lack profitable applications. In short, China AI is showing up most clearly in expectations for hardware resilience, not in chips or software. The infrastructure is being built, but the broader profit story has yet to materialise.

China AI is building momentum, but the earnings payoff remains uncertain

China’s AI ecosystem is buzzing with investment and experimentation – from hyperscalers building infrastructure to consumer platforms embedding AI into services. Yet outside a few areas, such as cloud and advertising, monetisation is still limited with most firms prioritising investment over returns.

Still, the long-run potential is meaningful. Morgan Stanley estimates that China’s AI investments may only break even by 2028, but could generate a 52% return on invested capital by 2030 with the broader ecosystem reaching US$1.4 trillion4. Over the coming years, the bank estimates AI could also add 0.2–0.3 percentage points to China’s annual GDP growth.

For investors, the trade-off is clear: investment is rising faster than monetisation today. The current chapter of China’s AI story looks to be more about building capacity and positioning for future growth than delivering near-term profits. With valuations still cheap versus US counterparts, however, the AI story can still drive further optimism – but for a sustained rally, earnings need to show.

Authors

Stephanie Leung, Chief Investment Officer

Stephanie and her team oversee the full spectrum of investment products and portfolios offered at StashAway. She brings more than two decades of investment expertise across multiple asset classes. Prior to joining StashAway in 2020, she managed investment portfolios at institutions such as Goldman Sachs and multi-billion dollar family offices in the region.

Justin Jimenez, Head of Macro and Investment Research

Justin has over a decade of experience in economic and investment research, and contributes to shaping the investment office's perspectives on the global economy and asset classes.

Glossary

Foundational models

Large AI systems trained on vast amounts of data that serve as the base for building specific applications. OpenAI's ChatGPT and Google's Gemini are examples of foundational models.

Open source models

AI models whose code, data, and training methods are freely available to be studied and built upon. This contrasts with proprietary models where companies keep their technology private.

Capital expenditure (capex)

The money companies spend on assets like buildings, equipment, and infrastructure. In the AI context, this includes spending on data centers and the chips needed to train and run models.

Hyperscalers

Firms that operate computing, storage, and networking data centers at a global scale. These providers deliver services through various models, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

Appendix

Analysis of earnings transcripts from Chinese companies on AI impact

{kind=link}

References

- Reuters. (2025). Alibaba, Baidu begin using own chips to train AI models, The Information reports. Retrieved from: https://www.reuters.com/world/china/alibaba-baidu-begin-using-own-chips-train-ai-models-information-reports-2025-09-11

- Reuters. (2025). China's Alibaba develops new AI chip to help fill Nvidia void, WSJ reports. Retrieved from: https://www.reuters.com/world/china/chinas-alibaba-develops-new-ai-chip-help-fill-nvidia-void-wsj-reports-2025-08-29

- McKinsey & Company. (2025). Data centers: The race to power AI. Retrieved from: https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/data-centers-the-race-to-power-ai

- Morgan Stanley. (2025). AI in China: A sleeping giant awakens. Retrieved from: https://www.morganstanley.com/insights/articles/china-ai-becoming-global-leader

Share this